A guest took our 2020 Jeep Wrangler off-roading in Hawaii. We told them not to. Turo’s terms of service explicitly prohibit it. They did it anyway, completely destroyed the engine, and left us with an $18,000 repair bill.

The guest violated the rules. We did everything right, filed the claim the same day the trip ended. We still paid $1,625 out of pocket.

Turo never reimbursed that deductible. It took 7 months and 8 different claims representatives to get the $16,365 they owed us.

That was under the old protection plans. The new ones are worse.

What Changed on January 7th

Turo consolidated their 5 host protection plans down to 3. They’re calling it “simplification.” What it actually means is higher deductibles at the same take rates.

The old structure (before January 7, 2026):

The new structure:

If you were on the 80% plan, your deductible just doubled from $750 to $1,500, and your earnings didn’t change at all. You’re just exposed to twice as much risk now.

If you were on the 85% plan like we were, that option doesn’t exist anymore. You either drop to 80% and lose 5% on every trip, or you jump to 90% and accept a $2,750 deductible. There’s no middle ground.

The 60% plan with the $0 deductible? Gone. Some hosts chose that plan specifically because they wanted zero out-of-pocket risk, even if it meant giving up 40% of their earnings. That choice no longer exists.

The Hawaii Claim

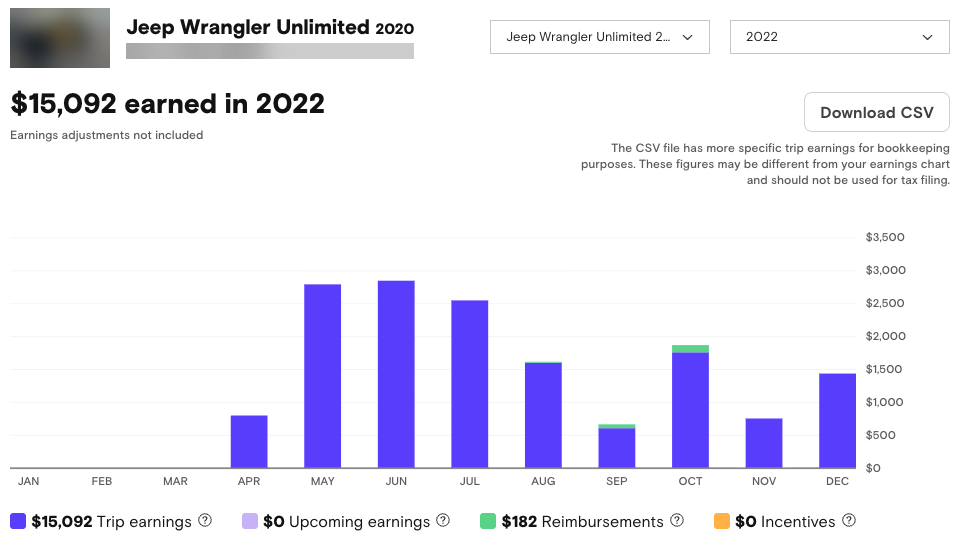

Our Jeep Wrangler had completed 59 trips over 15 months on the platform. It was one of the highest earners in our Hawaii fleet, averaging over $1,700 a month and hitting $2,500+ during peak summer months.

2022 was a strong year. The Jeep earned over $15,000 with peaks above $2,500/month during summer.

The trip in question was a 3-day rental. We earned $304.35 after Turo’s fees.

We always tell guests not to go off-roading because it’s against Turo’s terms of service, and we make that clear. If a guest asks about it, we tell them no and ask them to cancel if that’s their plan.

We found out at 1 AM when they messaged saying they had an “emergency.”

1:04 AM. “I went into emergency.” They were stuck on the side of a volcano in our Jeep at 1 AM.

We checked our GPS tracker and could see exactly where they were, clearly off-road where they shouldn’t have been (and why it is always at 1 AM???).

We called Turo, who arranged a tow truck. The Jeep went to a shop and the diagnosis came back four days later: full engine replacement required.

Then came 7 months of back and forth with Turo’s claims department.

They assigned our claim to 8 different representatives over those 7 months. Every time the claim changed hands, we had to follow up. Every “approval” seemed to lead to another approval stage. The claim was filed July 2nd, 2023. We didn’t see payment until January 27th, 2024.

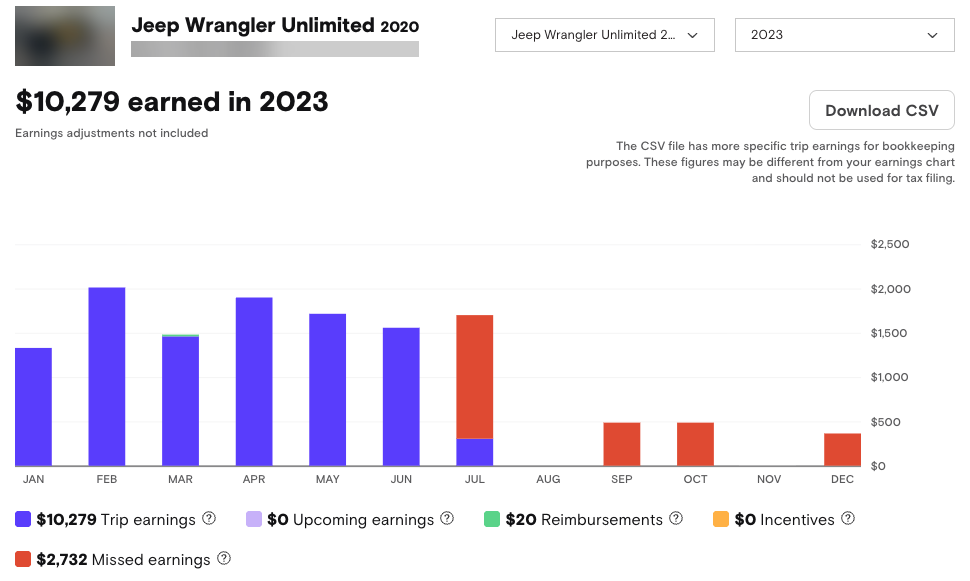

In the end, Turo paid $16,365.83 for the repair. We paid our $1,625 deductible out of pocket and never got it back (even though the guest broke the rules), and we lost 7 months of revenue from one of our best performing vehicles. Turo’s earnings dashboard tracked $2,732 in upcoming bookings we had to cancel, but the real loss was the entire peak summer and fall season where this vehicle would have earned $15,000 based on its historical performance.

Total financial hit to our business: $1,625 deductible plus $15,000 in lost revenue. $15,000 that we’ll never see, from a single 3-day rental where the guest broke the rules.

2023 tells a different story. See the red bars? That’s $2,732 in upcoming bookings we had to cancel. The blue earnings bars drop to $0 after July because the vehicle was in Turo policy limbo for 7 months.

A 3-day rental that earned us $304 cost our business over $15,000.

How the Deductible Actually Works

Most hosts don’t understand how Turo’s deductible structure actually works. After 10,000+ trips, this is what I’ve learned.

Both parties pay their deductibles regardless of who’s at fault.

If a guest damages your car, they pay their deductible (if they bought protection) and you pay yours. It doesn’t matter if the guest violated every rule in the book. You’re both writing checks.

Turo then pays for the repair and sends the guest to collections for their portion. If they collect from the guest, Turo gets their money back. Your deductible? That’s long gone. Turo doesn’t reimburse nor waive it, even when the guest clearly caused the damage through prohibited use.

Turo’s terms of service say guests who engage in prohibited uses “will be fully financially responsible for any related claims, loss, or damage.” Sounds like protection for hosts. In practice, it means Turo might eventually recover their losses from the guest. It doesn’t mean you get your deductible back.

And if you file through Turo, you’re not allowed to pursue the guest directly for your deductible. It’s against their policy. You have to trust Turo to handle recovery, and you have no claim to whatever they might recover.

You Can’t Even Say No Anymore

What makes all of this worse is that hosts used to be able to screen guests. You could look at someone’s reviews, read their messages, get a feel for whether they seemed trustworthy. If something felt off, you could decline the booking.

In early 2024, Turo made Instant Book mandatory. Every guest who meets their basic requirements can book your car automatically. You don’t get to approve or decline.

Turo says they screen guests using “a constantly evolving, machine learning model to assess risk.” In our experience running a 110-car fleet, that’s marketing language with no substance behind it.

We’ve had guests book whose previous reviews from other hosts explicitly mention crashing the car or damaging the vehicle. Turo lets them stay on the platform. We’ve had guests we’d never choose to rent to if we had the option, but we don’t have the option.

Turo is trying to grow market share, so they want as many guests as possible on the platform. The quality of those guests is the host’s problem.

The Risk Tax

Turo is shifting more risk onto hosts while taking away hosts’ ability to manage that risk.

The deductibles went up. The plan options got narrower. You can’t vet guests anymore. You can’t decline bookings that feel sketchy. And even when guests violate the terms of service, you’re still on the hook for your deductible.

Turo already prices for risk on the guest side. Younger drivers pay $30-50 more per day. Low-credit guests pay security deposits up to $750. Turo’s system assesses every guest’s “auto insurance score” before approval. On the host side? Nothing. Your deductible doesn’t decrease when you’re forced to accept a risky guest. Your take rate doesn’t improve. Turo charges for the risk they see coming. You just absorb it when it arrives.

Turo has also announced additional changes coming later in 2026, including variable take rates based on booking lead time and mandatory duration discounts. The details aren't final yet, but the pattern is clear.

What’s Already Changed (January 2026)

What’s Coming (Details TBD)

Turo announced these changes at their Fireside Chat but hasn’t released final details.

That last line in the table is important: mandatory duration discounts. Turo is requiring hosts to offer discounts on longer trips, and those discounts come out of your earnings, not Turo’s fees. When a guest gets 15% off a weekly rental, that 15% comes straight out of your pocket. Turo’s cut stays the same.

On a last-minute trip under the new variable rates, you’ll be paying for risk twice- Once through reduced earnings with the lower take rate, and again through the unchanged deductible at the higher risk rate. Turo’s exposure stays the same while they collect more from you on both ends.

I call it the risk tax, and hosts are the only ones paying it (twice!).

What I’m Doing With Our Fleet

We were on the 85% plan before January 7th, with the $1,625 deductible. That plan doesn’t exist anymore, so I had to choose.

For now, I’ve moved our Jeeps to the Balanced plan at 80% with the $1,500 deductible. It’s a 5% pay cut on every trip, but I wanted to keep our exposure manageable while I figure out the right long-term strategy.

I’m considering moving to Max earn at 90% with the $2,750 deductible because the math might actually work in our favor. Most of our claims are fender benders in the $500-600 range, and we usually resolve those directly with the guest without involving Turo at all. The catastrophic claims like the blown motor are rare and when we’d actually use insurance.

If you’re earning an extra 10% per trip, that adds up fast. On a vehicle doing $1,500-2,000 a month, you’re pocketing an extra $150-200. Over the course of a year without a major claim, that’s $1,800-2,400 in extra earnings, which is more than enough to cover the higher deductible if something does go wrong.

It’s basically self-insurance at that point. Save up a reserve, accept the higher deductible, and keep more of your earnings on every trip.

That math only works if you have the cash flow to absorb a $2,750 hit when it happens. If a big claim would break you, the lower deductible might be worth the peace of mind.

Common Questions

Did Turo grandfather existing bookings under the old plans?

Yes. Trips booked before January 7th keep the protection plan and deductible that was in place at booking time. The new plans only apply to trips booked after the change.

What happened to hosts on the 75% plan?

They got squeezed. The closest option is Max protect at 70%, where you lose 5% on every trip, or Balanced at 80%, where your deductible jumps from $250 to $1,500. There’s no good answer.

Can I still decline guests I don’t want to host?

Technically you can cancel trips, but Turo tracks your cancellation rate and it affects your standing on the platform. You can contact support in extreme situations but you’ll have to plead your case to a foreign Turo rep and hope they help you. The days of simply declining a booking request are long gone.

If a guest violates the terms of service, do I get my deductible back?

Based on our experience, no. We had documented proof that the guest went off-roading against our explicit instructions and Turo’s own rules. We still paid the deductible. Turo never reimbursed it.

Is Turo’s algorithmic guest screening actually working?

In our experience running a 110-car fleet, no. We regularly see guests with bad reviews and documented damage history get approved to book. Turo is prioritizing growth over quality control.

Is the 10% non-refundable discount mandatory?

Yes. As of January 20, 2026, all vehicles must offer a 10% non-refundable discount for trips booked 4+ days in advance. Hosts cannot change the percentage or opt out.

I run the financial operations of a 110-car Turo fleet remotely from the beach in Playa del Carmen, Mexico.